Un nuovo grande rischio Lehman Brothers aleggia su mercati ed economie

Io sono ovviamente speranzoso che la Gran Bretagna non esca dall’Unione Europea. Al momento i sondaggi sono ancora favorevoli al Brexit, manca una settimana esatta al voto, vedremo come va a finire. Intanto però, come ho previsto (non perché ho la sfera di cristallo ma perché era ovvio) il sistema finanziario inizia a muoversi e cerca di far capire agli inglesi che il voto “di pancia” potrebbe portare danni enormi.

Uno dei pareri più autorevoli che ho letto nelle ultime ore (lasciando da parte politici ed i soliti noti) è quello di Hung Tran, direttore dell’istituto di finanza internazionale IIF a Washongton. Autorevole e…decisamente aggressivo… un parere realistico oppure eccessivamente pessimistico? Nessuno lo può dire, non ci sono precedenti a cui possiamo aggrapparci. Secondo me c’è il concreto rischio che il suo punto di vista sia molto vicino alla realtà.

In un interessante Q&A, ecco il parere di Tran, apparso ieri su Bloomberg.

Q: What would happen if Britain voted to leave the EU?

A: It is not Lehman Brothers in the short term in terms of markets being in a panic or chaotic mood, because the central banks will try to pacify that. But it is more significant than Lehman Brothers in its longer-term impact on global growth. Through trade and investment channels, there will be a downward impact on growth.

STOP: già qui una dichiarazione a vetriolo. Le banche centrali interverranno per evitare un “effetto Lehman” nel breve ma nel medio lungo termine, una Brexit avrebbe addirittura effetti più pesanti. Cavolo! Mica male, soprattutto se ragioniamo su un modo dove la leva finanziaria regna sovrana, dove tutto è programmato e non sono ammessi scenari alternativi soprattutto se destabilizzanti. Quindi il mercato non sarebbe assolutamente pronto ad assorbire la Brexit e gli effetti sarebbero devastanti.

Q: Isn’t it just a European issue?

A: It’s not just a vote for the U.K. exiting Europe, it is a symptom of the discontent and unhappiness of citizens with the status quo. They want change, but nobody can articulate what is it that they want. The impact in an exit vote of “leave” winning would be very far-reaching and impact long-term events. Near term there would be significant adjustment in financial markets.

VERO: il voto della Brexit è un voto di protesta. I cittadini inglesi, ma anche quelli europei, sono insoddisfatti e stufi. MA questo è il classico “voto di pancia” che può avere conseguenze pesanti se non viene ponderato correttamente.

(…)

Q: Which countries would suffer most if the U.K. voted to exit?

A: First the U.K. and Europe, but then emanating from there to trading partners of Europe, and then to emerging market countries through the decline in world trade. Large economies able to rely on domestic consumption and the services sector should be able to generate a measure of growth and cope with it better than others. More open economies that have been reliant on world trade as a growth model will suffer more.

ECCO FATTO: è una follia chiudere gli effetti di una Brexit all’interno delle mura inglesi. Ma anche europei. Sarebbe un evento sistemico che colpirebbe ovunque, mercati emergenti compresi. Ricordate quando vi parlavo di un sistema che sta in piedi “con lo sputo” e che non avrebbe retto un problema sistemico inatteso? Eccovi serviti.

Q: What happens to the U.K. after exit?

A: Whatever new arrangement the U.K. may manage to have — the Norway model, the Switzerland model, or relying on the WTO to manage its relationship with the EU — is very problematic. All of those still require U.K. firms to observe and respect EU rules if they want to do business in the EU. Most important for the City of London, financial services passporting will be either not available or significantly curtailed.

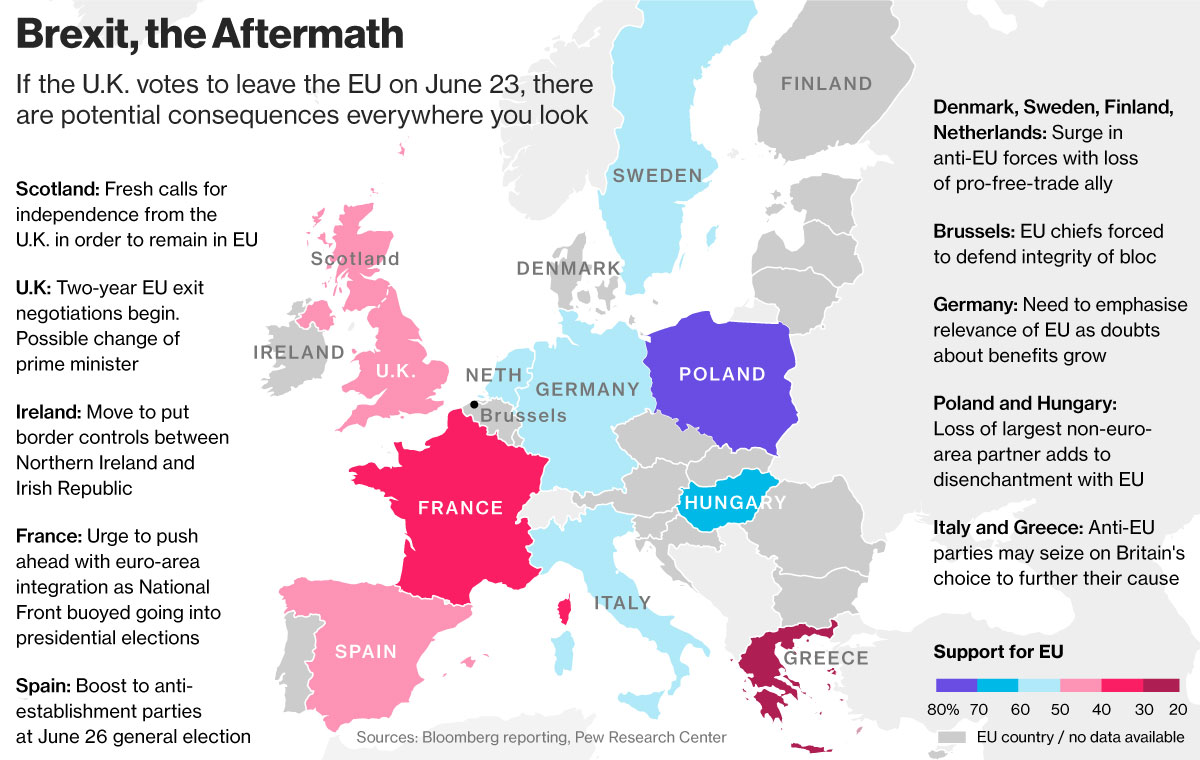

LA QUESTIONE POLITICA diventerebbe il vero problema,ancor prima della rinegoziazione degli accordi commerciali. La Brexit darebbe il via alla Euro-disgregazione. La mappa sottostante traduce in modo esemplare questo rischio.

Q: What’s the U.K. economic impact?

A: The true problem is uncertainty causing loss of business confidence and further decline in capital expenditures and investment. That would reinforce the collapse in productivity — which is very pronounced in the U.K. — and make for an even worse outcome in terms of potential growth.

Q: How does it affect the EU?

A: If you put the Brexit vote against a very clear decline in trust and confidence of the citizens of Europe in the EU and its institutions, and the rise in populism and anti-Brussels, anti-EU, anti-integration sentiment, the contagion risk of a successful Brexit vote will be quite damaging. Periphery countries have undergone a lot of adjustment after the crisis. The cost of fiscal consolidation is perceived to be quite significant and unfairly distributed, so there could be a lot of discontent, and that will support the further rise of populist political movements.

Q: What does Brexit mean for trade?

A: The mood is anti-immigration and anti-free trade. In the past year, more than 500 trade protectionist measures have been implemented by governments worldwide, more than twice the number of such measures two years ago. Against ths anti-immigration, anti-free trade public mood — even here in the U.S. — the risk of a further increase in trade protectionism is high. That would continue to depress the growth of world trade, which actually fell in volume terms by 1.6 percent, year-over-year in the first quarter.

TRE DOMANDE di cui è difficile dare delle risposte ma ne abbiamo già parlato nei giorni scorsi. Sarebbe un gran problema. Molti lo stanno sottovalutando (proprio perché sono portati a ragionare”di pancia”) ma sappiate che…porterà conseguenze molto pesanti.

Ripeto, nessuno può sapere con esattezza cosa accadrà, Ricordatevi solo di queste parole. Gli effetti di una Brexit saranno peggiori del default di Lehman Brothers. E’ un parere di un grande esperto (citato nel post) ma non si allontana nemmeno troppo da quello del sottoscritto (ed è per questo che ve l’ho proposto).

Riproduzione riservata

STAY TUNED!